This is a topic I’ve addressed more than once on this blog. But it’s so important, I feel like doing it again. Today I saw a post on The Deal Mommy about her family’s scary experience in Gran Canaria, Spain I recommend you read it, but here is a short version: her husband suddenly felt sick and had to undergo surgery in a foreign country to the tune of 4,500 euro, which had to be paid upfront. The trip insurance which cost $38 should cover it, but more importantly, they didn’t have to agonize over the decision of whether to seek medical treatment or not. And now they can enjoy the rest of their trip with a father who is still alive.

I’ve written posts on benefits of medical insurance here and here The second post focuses on how I purchased a medical-only coverage for $10 on a 3-day trip to Jamaica and almost had to use it. Many times you can get away with a “bare bones” coverage, especially if your flights (or award ticket taxes) are paid for with a card like Chase Sapphire Preferred. Some products, Citi Prestige comes to mind, even provide medical evacuation.

However, for most expensive trips, I recommend a more comprehensive insurance. The cost will most likely be quite small compared to the overall amount. While a credit card may give you one or two important benefits, it’s unlikely it will provide all of them. For me personally, when I buy travel insurance, I focus on three areas: Medical coverage, evacuation and trip interruption. All other benefits are just the icing on the cake.

Let me give you an example. In a few months, we are going on Alaska cruise. I would never consider doing it without a travel insurance. Not only will it protect me in case we have to cancel, but we will have medical coverage for hospitalization in Canada and medical evacuation benefit if one of us has to be airlifted off the cruise ship.

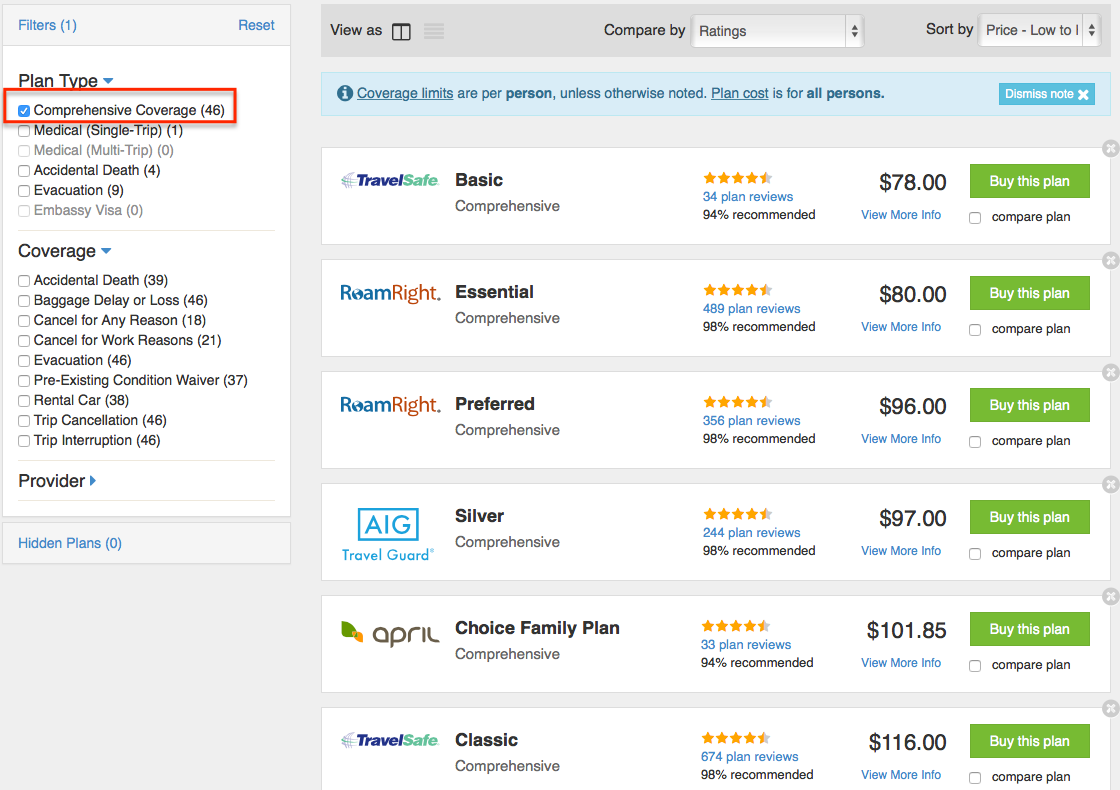

Let me show a quote for 4 people: 2 adults and 2 kids. Total cost to insure is $4,000. The site I recommend is Insuremytrip, IMO the best one-stop resource. After you fill out all the details, select “comprehensive coverage” and sort the results by price:

Let’s compare five plans:

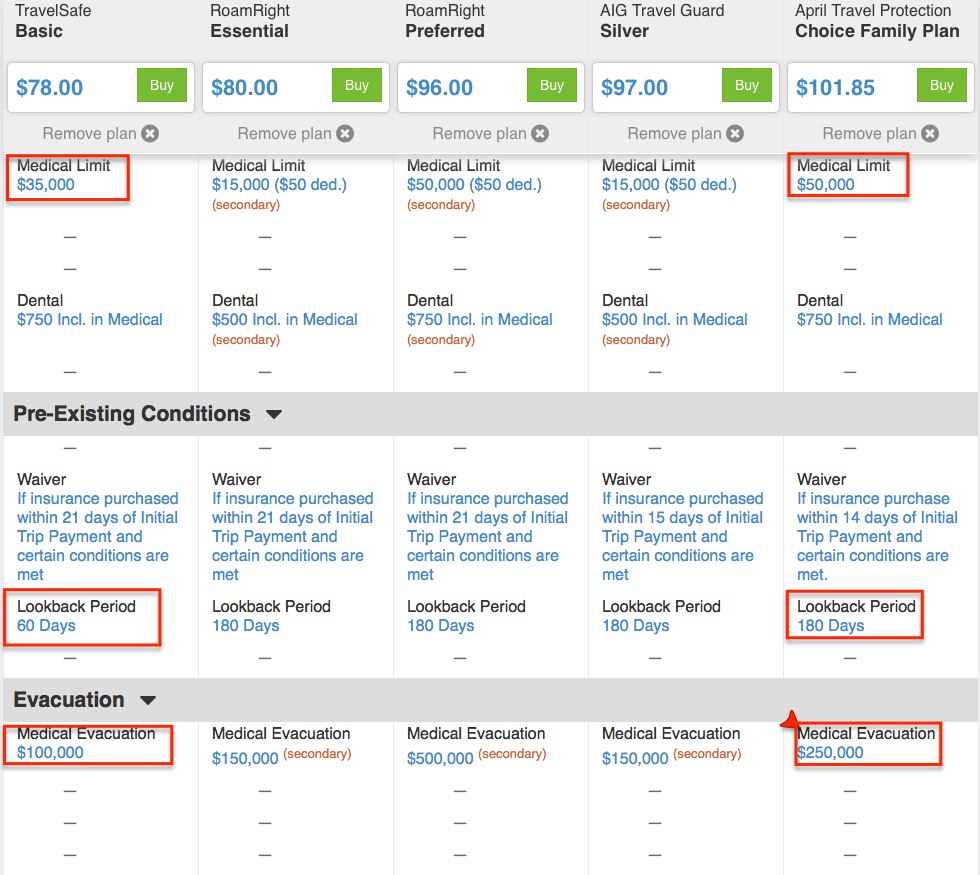

The cost is total for all 4 travelers, and limits are per person. If at all possible, I recommend you try to buy a plan with a primary medical coverage. That way, you won’t have to deal with your own health insurance in case something goes wrong. This is especially important if you happen to have a high deductible plan like I do. Personally, I like to have at least $50K in medical coverage per person, so would pick the most expensive option.

Medical evacuation limit on it also happens to be higher, but I think that $100K would suffice, so this wouldn’t influence my decision. There is one advantage to the cheapest plan: 60-day instead of 180-day lookback period when it comes to pre-existing conditions. If someone in your family has had medical problems in the past and you happen to buy past “waiver” time period, this is something to take into account.

Incidentally, “trip interruption” benefit on the more expensive pan is $1,500 per person compared to $1,000 on the cheaper one. Here is the definition in case you don’t know what I’m talking about. Basically, if your parent back home suddenly gets sick and you need to cut your trip short and fly back, this benefit will pay for it.

This is something a few premium credit cards will take care of, but it’s nice to have that extra layer of coverage. Personally, I believe it’s better to over-insure than to under-insure. Once again, we are talking about paying $100 to protect a $4,000 purchase and potentially your entire emergency fund in case things go very wrong .

When my parents come here to visit us, I always buy them a 1-million dollar health insurance coverage. It costs me around $140 for both each time, but I consider it money well spent. During our last trip, my mom got stung by a jelly fish and her leg started to swell. The swelling did subside and she was fine by the end of the day, but I had the peace of mind that we could take her to the emergency room if needed, and that we wouldn’t be on the hook for a $2,000 bill afterwards. When your loved one is sick, the last thing you want to think about is money. So take care of your trip insurance before the trip. Just do it.

Click here to view various credit cards and available sign-up bonuses

Author: Leana

Leana is the founder of Miles For Family. She enjoys beach vacations and visiting her family in Europe. Originally from Belarus, Leana resides in central Florida with her husband and two children.

What would you do if you are traveling home on separate dates? Should I get a policy for two and a separate one for the three of us staying a day later? Also, I only paid $1000 for flights, the rest was points. Would I count only $1000 as my expense? How do you price out the vacation? Only what you paid so far or what you will pay? For example, I’ll have the airfare and Airbnb paid for before our trip. I only get the rental car upon arrival. Do I include it? Thanks for your help.

@Michelle I would buy two separate policies, yes. The insurance companies base coverage on dates. As far as award tickets go, that’s a bit of a grey area. Many companies will pay mileage redeposit fees, so check the fine print. But the short answer is yes, I would count $1,000 for flights. Also, I would count future estimated costs when buying the policy. The companies know that some expenses will have to be paid later, so it’s fine. Of course, always check the fine print, just in case.

As someone with almost 20 years in the insurance industry (three different insurance companies) I’d say just go with the best deal. Insurance is highly regulated and they are kind of all the same. My experience is that most “horror” stories come from people who don’t understand their policies so they are mad, stressed, disappointed. Most insurance workers work by the book and are much happier paying claims than denying them. Denying them is a lot more work and a lot more stress when the customer is angry. But they can lose their job if they pay an illegitimate claim. The rules are the rules and the contract is the contract.

@Amanda Thanks for chiming in! Nice to hear from an insider on this particular topic. I usually look at the price as well as benefits. If the reviews are mostly positive, that’s good enough for me.

Hi Leana, a question – what are your thoughts about the various companies providing travel insurance? I need insurance for an upcoming 6-week trip to New Zealand/Australia and April was by far the cheapest option. However when I read its reviews there were quite a few negative ones. I know Dia uses

Allianz and has also mentioned TravelGuard. Of those two Allianz is definitely cheaper, although it doesn’t include accidental death coverage (makes me sweat even thinking about it). Just wondered what, if any, your experiences (though sounds like you’ve been lucky enough not to have any), or those you’ve heard about, have been. Thanks!

@Audrey I actually had to make two claims with Travel Guard insurance. Nothing bad to say, everything went smoothly and they paid out as promised. I did buy Allianz once, but everything went well during that trip, no claims. I do trust Dia’s recommendation, and I wouldn’t worry about accidental death coverage. If you have good life insurance, it’s fine to skip it.

I’m not familiar with April Insurance company, but I did just buy their policy for our Alaska cruise. To be honest, I didn’t even read reviews. Overall rating is pretty good, so that was sufficient for me. Maybe I should have done more research, who knows? I think if you dig deep enough, every company will have a horrendous story from one of their customers. The thing is, it’s impossible to know whether this person is telling a complete story. If all reviews are bad, that’s a red flag, of course.

Obviously, I can’t tell you what to do. This is a big trip, so maybe it’s better to go with Allianz since it’s highly recommended by Dia. She made four claims with them, and they paid out each and every time. So, it comes down to what you are comfortable with. Hopefully, you’ll never have to find out whether the company is solid or not!

Thanks Leana. I did see you highlighted April in your post, so thought I’d ask. I agree that you can always find complaints, but some companies definitely had more negative feedback than others. As you say, it’s a big trip, so I’ll probably end up going w Allianz to be on the safe side. Not worth saving even $20 if I’m risking more hassle – kinda defeats the purpose!

No problem! I hope you’ll have an uneventful trip.

If you use miles for the airfare and points for hotels, what do you use as the total trip cost?

@Rich That’s a tough one! I actually faced this dilemma with our Jamaica trip See this post https://milesforfamily.com/2015/03/26/why-you-should-be-a-tortoise-when-it-comes-to-travel-insurance/ So, I ended up just getting a medical-only policy, which I strongly recommend. Usually, the company will only reimburse you for your non-refundable expenses. If you have Chase Sapphire Preferred, reportedly, it will cover trip interruption even if you got award tickets. See the post I’ve mentioned, there is a link to VFTW overview of this subject. There is a separate benefit you can buy, which will cover award tickets.

Hi, sorry, i contra get the cost, you talk about $100 and $4000. How much did you pay for the insurance for the four of you?

Leticia, it cost $100 total to insure all four of us for a 7-day Alaska cruise. The amount is for $4,000 total, $1,000 per person. So, if something goes wrong before the trip, we will get reimbursed all the non-refundable costs. It also includes medical and evacuation coverages during the trip. I think it’s a fair price to pay to have a peace of mind.